Exploring Probability and Options Expiration (WULF)

Exploring Probability and Options Expiration (WULF)

Hello friends and subscribers. It has been a while (4 weeks) since I have sat down and actually committed myself to writing anything serious. For a while I took a break as I was a bit out of ideas and on top of that I think my alcohol recovery has played a weird role. One of the things they don’t tell you about alcohol recovery is you go through tough periods where the things that you used to take interest in no longer have meaning and it becomes very difficult to care about anything. This is largely due to the chemical change and rewiring of your brain. It sort of made me second guess myself. Like, am I doomed to Ray Charles fate when he quit using? No junk no soul as they say. I got over it, but it took a bit longer than I thought. I still care immensely about trading and that cannot be killed by my brain changing itself against my will.

Alright so moving into another topic on probability. I was scoping out some options on e*Trade and brought up their options analyzer tool. I noticed at the bottom that there was a probability calculation to determine the likelihood of an option expiring “In The Money” (ITM) and “Out The Money” (OTM). I decided that this should be my next topic of learning and writing so I decided to explore the arena a bit.

In this study I am using options for the stock WULF. A smaller cap bitcoin mining stock with a decent selection of options, WULF will serve our purposes well here.

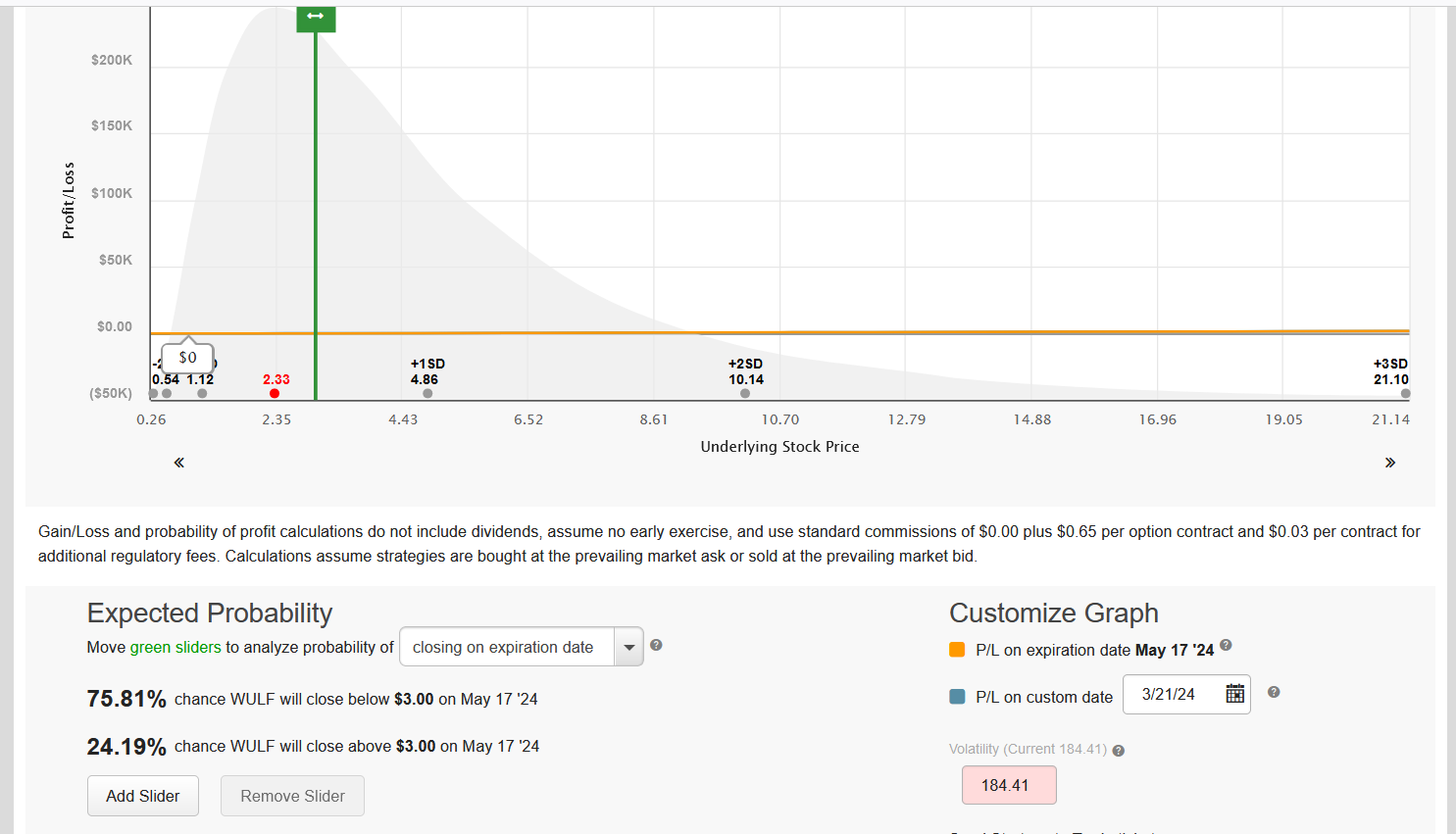

This is the data provided by e*Trade options analyzer tool. The probability (denoted %P) of an option being ITM will sometimes also be worded as the probability that a stock will close above or below a certain price. If you have one probability (ITM or OTM) you have the other.

Instead of including a photo of the options analyzer tool for every single strike and expiration I just compiled it all into a table of data for simplicity sake. However, notice how the distribution in the background changes with profit and stock price. This is a clue to how this probability is calculated, however, I do not know the exact formula they are using to calculate this probability but mostly just a well informed guess.

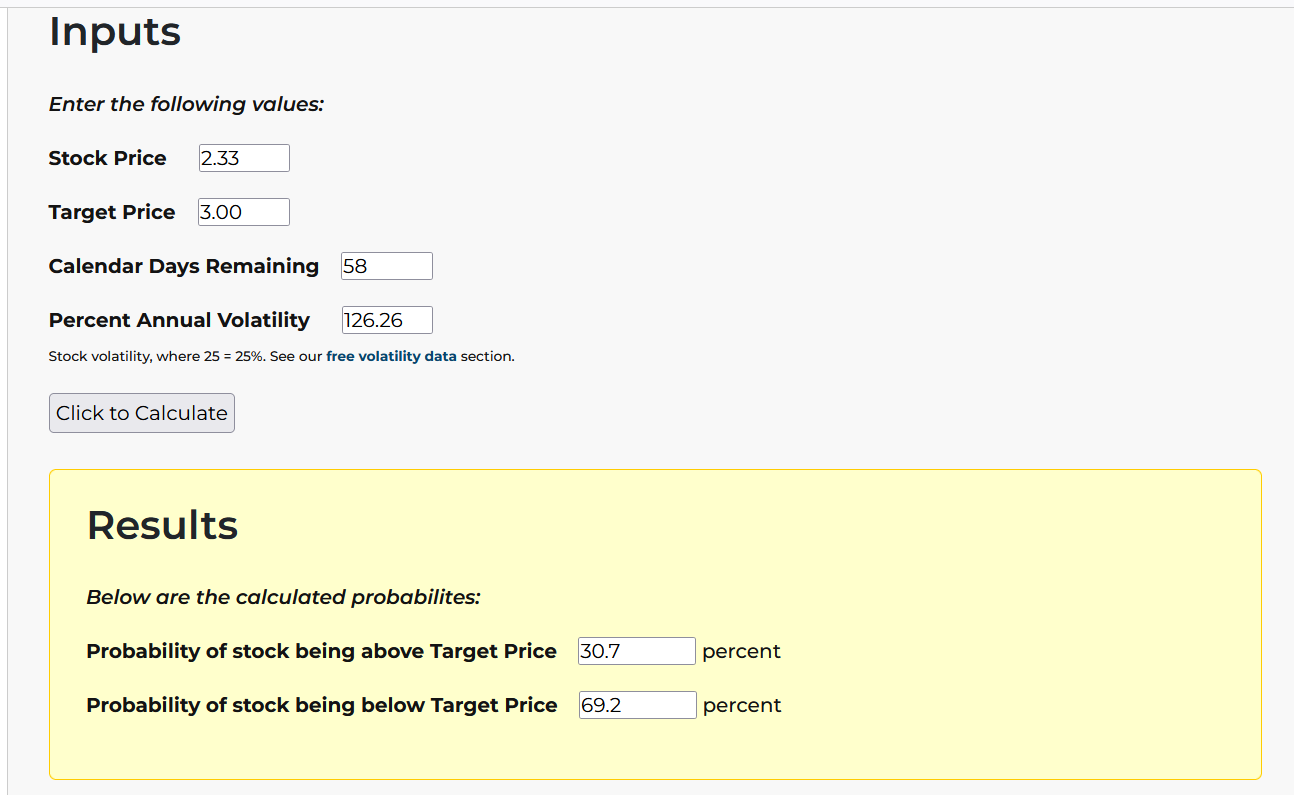

Below I compiled this data using an online calculator https://www.optionstrategist.com/calculators/probability and it is very noticeable that they do not align in absolute congruency with the probability data given by eTrade. Which one is more to be trusted or more accurate? I hope to answer this question a bit down the line. For now, make sure to notice some of the trends such as a decreasing probability of being ITM with higher strikes. The photo below is from Wednesday’s price data and the data below is compiled after the market closed for the weekend on Friday.

I have previously written a bit about the Black Scholes options model and how I got the number 126.26 above is what is called annualized volatility (I believe). It could be that I am using the wrong type of calculation for this input. That is possible. Etrade gives a number of 170-184 for this and it seems to fluctuate more than what I have. This is certainly part of the reason why there is error between Etrade numbers and what I got using the optionsstrategist website.

Something I noticed immediately between the May 2024 options and the August 2024 options is that probability decreases more for the longer out August options than for the closer May options. I was very curious about why this is. It does not exactly matter rather we use eTrade’s data or the optionsstrategist data. They both have a lower probability for the strike $2 expiring in August than for the $2 call option expiring in May. I was curious about why exactly this is the case, and to be perfectly honest, I don’t know I have the right answer. However, I think that it has to do with the distribution of a bell curve. A bell curve is a distribution that is symmetrical about the mean. So that means that either direction up or down that the stock travels in price brings it further away from the current price which these probability models assume is random and static. These models assume that when a stock is at a given price it is most likely to remain at that price and that extreme movements up or down are less probable than nonvolatile moves. Let’s continue with the August 2024 options data.

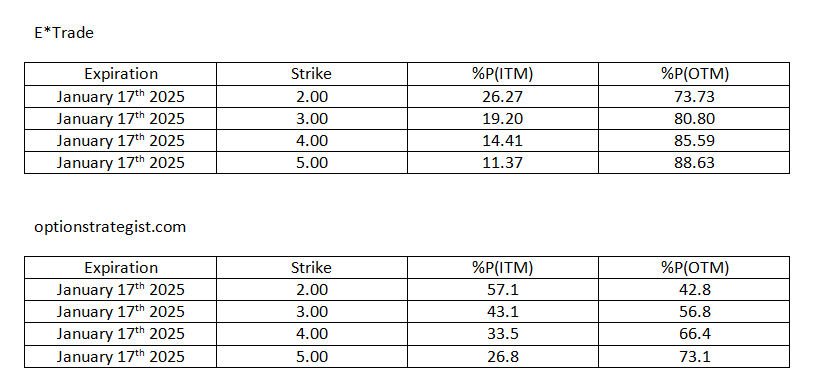

Ok, so the first thing I notice is the difference in probability results for ITM strike $2 between the etrade data and the optionsstrategist data. The gulf between these two results becomes even larger when we move further down to the January 17th 2025 options. Likewise, when we move down to the January 2026 the difference between these two results becomes even larger. From what I read on the options strategist website is that they are possibly using something called a Monte Carlo simulation. A monte carlo simulation is a specific statistical function that is actually beyond the scope and complexity of what I am trying to do here today and now, so we will have to explore monte carlo simulations further down the road. It is highly likely that the eTrade options analyzer is not using or including a monte carlo simulation and this is contributing to the difference between results for the two of them. For now, I am going to try and remain to the topic of probability of ITM or OTM options for WULF stock. Going to move on for now and explore the January 2025 options.

I think that we can be relatively certain that the variable functions or inputs involving these probability calculations are limited to current stock price, strike price, time to expiration, and volatility. These probability calculations do not involve what candle sticks are there. There is no accounting for company fundamentals, investor sentiment, or any other type of analysis. This means that these probability functions would fall under the category of classical probabilities although because that annualized volatility is a frequency function there is also a mix of both classical and frequency probabilities.

So for the probability data given by the eTrade results; I am somewhat skeptical here as the probabilities just look so low and somewhat unrealistic. I accept that it is simply what the equation has produced and that equation does not account for my feelings or emotions or any otherwise scowling curiosity. To revisit one of the questions I postulated earlier, should we place a greater trust in the eTrade options analyzer data or the optionsstrategist.com data? Honestly, I think the optionsstrategist.com data is actually closer to reality but I still have not looked underneath the hood at either formula specifically. Take all of these probabilities with a grain of salt and a healthy dose of skepticism.

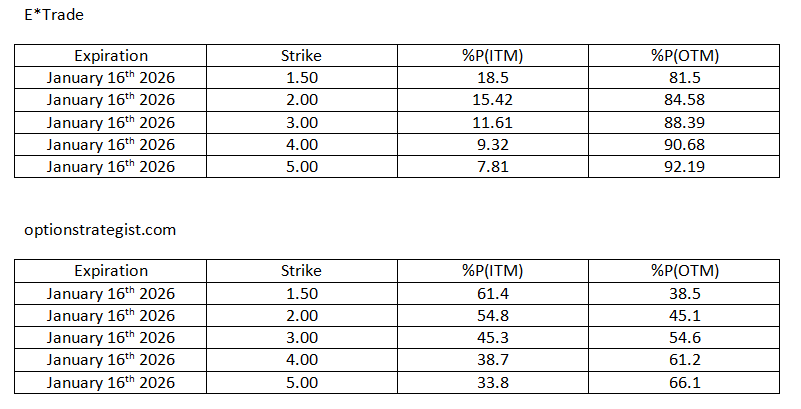

Let’s start to wrap things up here with a final look at the January 2026 options.

Notice in the eTrade data above how the probability of the January 2026 strike $1.50 option being ITM is only 18.5% despite the fact that it is already ITM by about 1.00? I managed to pick up a few of these options for 0.97, which means that should WULF stock be at this price ($2.46) on January 16th 2026 my contracts could be executed for breakeven. The added benefit of those contracts having approximately another 660 days till expiration I believe makes the probability of them expiring ITM all the more likely. For this reason I think the optionsstrategist calculator is maybe a bit more realistic and should be more acceptable with an ITM probability of 61.4%.

So how am I going to wrap this up? Let’s keep in mind that these probability calculations are not perfect substitutes for saying that the probability of a stock will be at a certain price by a certain date. Theta or “time decay” plays a big part in these calculations and that means it is not directly translated to the probability of a stock being at a certain price.

I want to encourage everyone to sign up for my substack if you haven’t already. This is often the subject matter that I write about. I try and always explore new arenas and topics that most other traders ignore such as hard math and statistics. I try my best not to make it too complicated for the average trader to understand. I also make every effort to make sure what I write is more so focused on quality rather than quantity. I likely won’t write every single weekend but hopefully when I do the reader has learned something they can’t get elsewhere.

Some topics I hope to be exploring in the near future: I knew there was some statistical topics out there that deal with risk management and have some sort of mathematical function. I think I have found this and I will be exploring this in the future. I am also looking at alcohol related stocks for a possible short trade. It’s not just me that is heading down the sobriety road. I think there are lots of other millennials here in America that have come to realize booze is not cool like it used to be. I am sort of looking into some of the equities related to hard liquor but still haven’t gotten around to it.

Today is Sunday March 23rd 2024 and this is a short trading week as the NYSE is closed on Good Friday for a holiday. Have a great short week traders.